What is a covered bond? Perhaps that is the logical place to start for many before dealing with offerings and policy and issues. See What are Covered Bonds.

See all the data on U.S.$ and Canadian bank covered bond activity since 2007 at Data Tables.

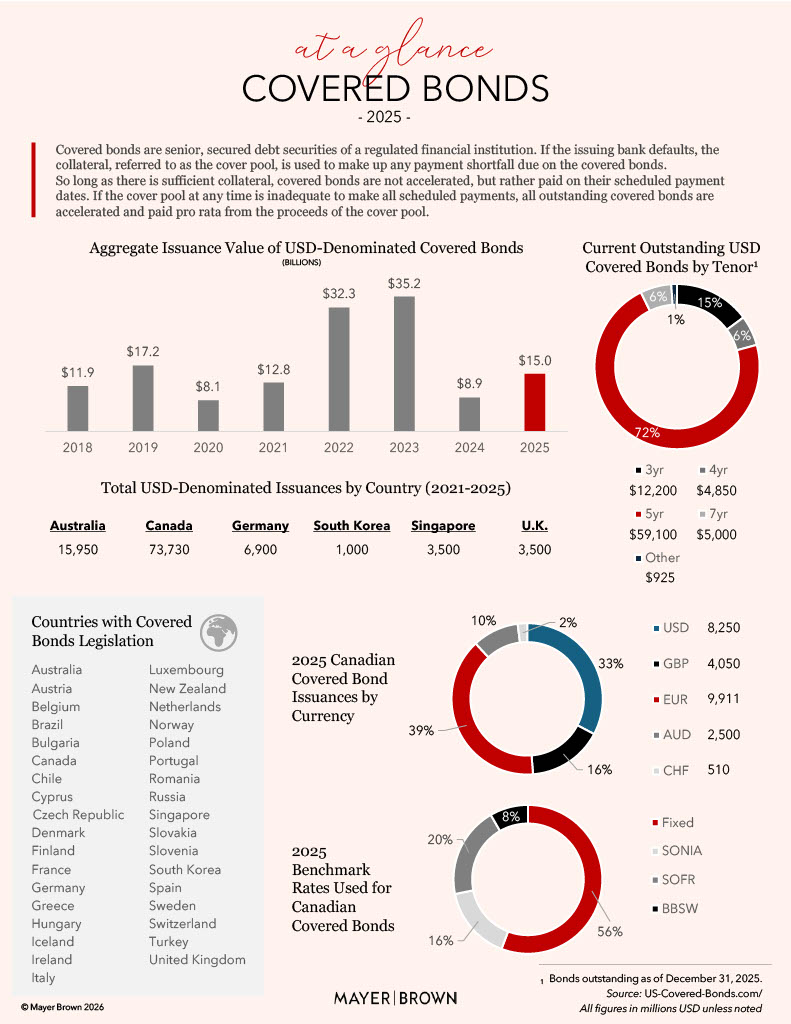

See Mayer Brown’s Covered Bonds – At A Glance for U.S.$ covered bond statistics for the period 2010 through 2025.

Commentary

Jan 2025- Reg AB II – President Trump has nominated Paul Atkins to be the next Chairman of the SEC. Paul was previously a Commissioner at the SEC from 2002 to 2008. There is talk that the new Chairman wants to address the Reg AB II changes that require residential mortgage securitizations (RMBS) to provide loan level disclosure for 273 data items for each loan in a securitization pool. As a result of those requirements, no new RMBS offerings have been registered with the SEC since the changes became effective in 2016.

This effort ties into the new administration’s goal of removing the GSEs (Fannie Mae and Freddie Mac) from receivership imposed on them in 2008 during the financial crisis and privatizing them. There is a concern that privatization cannot be accomplished unless there is a strong private sector mortgage market and SEC registered RMBS is felt to be a critical part of that.

Note that relaxation of the loan level data requirements for SEC registered RMBS could also open the possibility of restarting the SEC registered covered bond programs the Canadian banks abandoned in 2016.

Jan 2025-A New Administration – eight years later another Trump administration. What does it mean for covered bonds? Obviously way too early to tell. Once again we are hearing that the administration intends to move to address Fannie Mae and Freddie Mac. However, too early to know if covered bonds will play a role in any housing finance system, but we will be following closely.

Jan 2019- The American Banker is reporting that “There’s now a confluence that’s been built around the need to really do a deep dive on national housing policy itself, which housing finance is just one important element,” according to David Jeffers, the executive vice president of policy and public affairs at the Council of Federal Home Loan Banks.

Jan 2019-Urban Institute Report on U.S. Housing. See our new post (U.S. Housing Overview.) on the Urban Institute Report on U.S. housing and the dominance of the GSEs in housing finance. The GSEs are virtually the only game in town. Is that risk to the taxpayers worth it? Why?

Dec 2018- NY Fed Study on Housing Finance The New York Federal Reserve Bank has released an Economic Policy Review entitled The Appropriate Role of Government in U.S. Mortgage Markets. Given the conservatorships of Fannie Mae and Freddie Mac, one wonders why it took so long to ask this question. Nevertheless, this review represents a welcome attempt to inject some rationality into U.S. housing finance. As the Economist reported yesterday, we have accidentally nationalized the U.S. mortgage market at a cost of something like one percent of GDP annually. It is high time to rely more on the private capital markets and less on government fiat for housing finance. The Economist believes the taxpayer savings would be substantial.

Starting on page 63 there is a comparison of U.S. and Danish mortgage financing and a recommendation that policy makers look at the Danish use of capital markets to finance mortgage loans using covered bonds.

Jul 2018- GSE Progress? The White House has proposed a plan for reorganization of the Government, which includes a plan for reorganization of the GSEs that has a political twist that might actually make a difference. “Reform of the Federal Role in Mortgage Finance” begins on page 79 of the White House proposal. The plan would fully privatize Fannie Mae and Freddie Mac and give them access, together with other private entities, to a Government guarantee for a fee. Under the plan a new Federal entity would create and regulate a market for Federal guarantees.

The interesting political twist is that Fannie Mae and Freddie Mac would not longer be responsible for assisting low income borrowers. Instead that role would shift to the Department of Housing and Urban Development. Fannie and Freddie would lose their Federal charters and would no longer be the focus of political infighting over federal assistance for low income residential mortgage loan borrowers. Perhaps with the removal of that responsibility Fannie and Freddie will become less political and some real progress could be made in creating a rational structure for providing Federal support for residential mortgage loans.

Jan 2018- What a difference a year makes! – As we move into 2018 there isn’t a whisper of covered bond legislation in the United States. Nothing! The resurrection of the GSEs in their old form seems to be on the agenda. Amazing how short memories are. All is forgiven. $180 billion of bail-out cash is no big thing. We could do it again if need be, but of course this will never happen again. Everyone is born again! And what is the definition of “madness”?