A New Narrative

A lot of ink has been spilled assigning liability for the financial crisis to sub-prime mortgage loans.The role of sub-prime mortgage loans was so prominent that it has been called the ‘sub-prime crisis’. But a recent study by the New York Federal Reserve Bank shows how wrong this conclusion is.

In a paper published on Liberty Street Economics, “Did the Subprime Borrowers Drive the Housing Boom?” the authors demonstrate quite clearly, for example, that inflated appraisals were not concentrated in sub-prime mortgages.

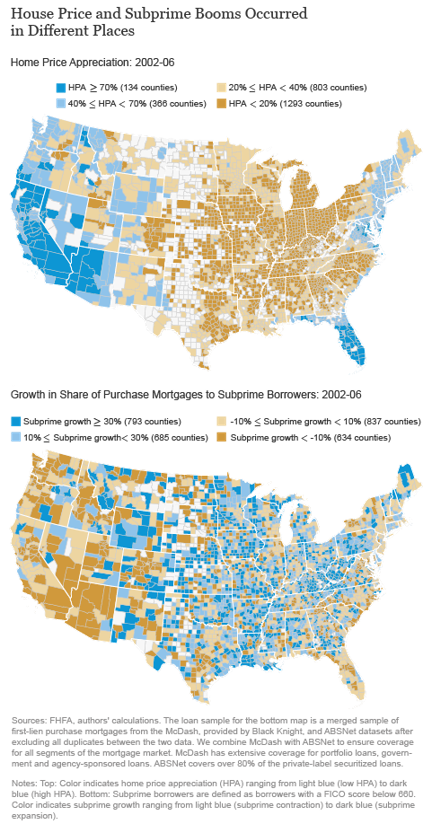

They also demonstrate that the boom in house prices and sub-prime mortgage loans occurred in different places (see the maps below). They show a clear negative correlation between house price appreciation and the sub-prime share of home purchase mortgages.

As the authors say, “Our analysis contributes to a ‘new narrative‘ that rapid U.S. house price appreciation during the 2000s was mainly driven by prime borrowers. Hence, policy prescriptions intended to limit access to credit for marginal borrowers may be insufficient by themselves to prevent a future housing boom.”